Rich Dad, Poor Dad – Book Summary

Rich Dad, Poor Dad – Book Summary

What the Rich Teach Their Kids About Money – That the Poor and Middle Class Do Not!

Robert T. Kiyosaki

Plata Publishing (11 April 2017)

About Robert Kiyosaki

Robert Kiyosaki has challenged and changed the way tens of millions of people around the world think about money. He is an investor and entrepreneur with an estimated net worth of over $80 million. His Rich Dad brand has published more than 15 financial self-help books, which have sold over 26 million copies worldwide.

About The Book

“Money is one form of power. But what is more powerful is financial education. Money comes and goes, but if you have the education about how money works, you gain power over it and can begin building wealth. The reason positive thinking alone does not work is because most people went to school and never learned how money works, so they spend their lives working for money.

Because I was only nine years old when I started, the lessons my rich dad taught me were simple. And when it was all said and done, there were only six main lessons, repeated over 30 years. This book is about those six lessons, put as simply as possible, just as simply as my rich dad put forth those lessons to me. The lessons are meant not to be answers, but guideposts that will assist you and your children to grow wealthier no matter what happens in a world of increasing change and uncertainty.”

Did you learn about money in school? Me neither ☺ We learn all different things (and many of them are not even applicable to our day to day life), but financial literacy is left behind. Money is a big part of our life, and it is really helpful to become wise about it.

If you are looking for your way to financial freedom, want to know how money works and how rich people think, this book is a great starting point. And here you can get all the big ideas about money that you should teach your children from a very young age. The book is packed with insights, but we’ll cover just a few in these notes. Let’s jump straight in.

Key insights:

The Rich Don’t Work For Money.

“The poor and the middle class work for money. The rich have money work for them.”

Two basic emotions drive our decision-making – fear and greed. If you have money, you are more likely to focus on all the things it can buy (greed). And if you don’t have it, you probably worry you might never have enough (fear).

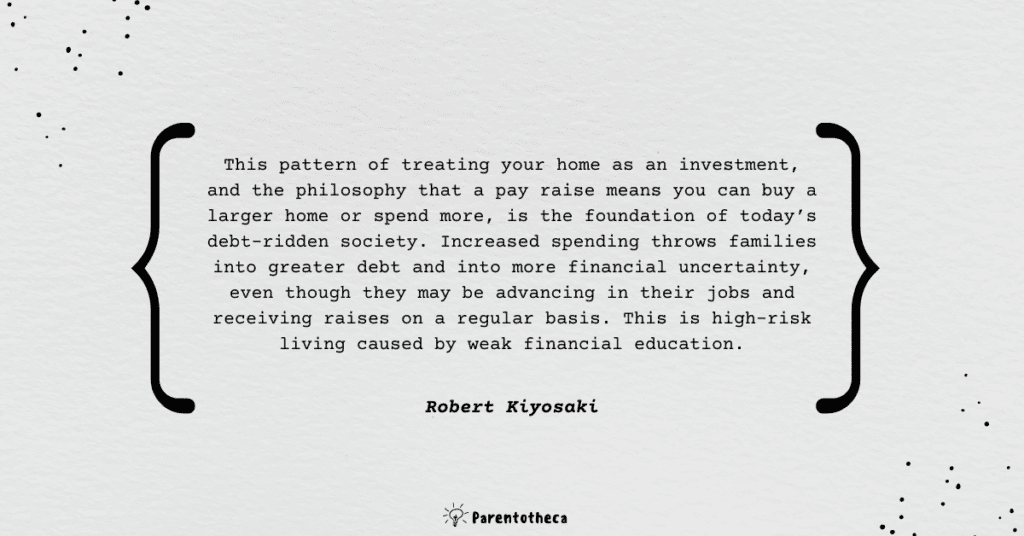

Here is how it works. Let’s say you received a generous pay rise. You have two options here: invest the extra money into something like stocks or bonds so that you could earn more money later over time, or you can spend it on something to upgrade your quality of living (like a car or a house).

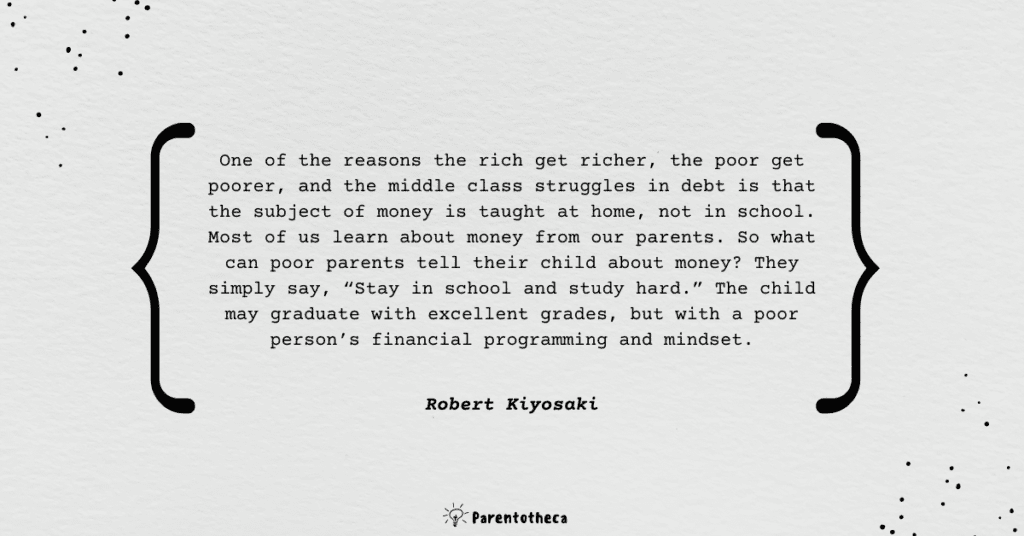

So if you are financially illiterate, your fear of losing the money will prevent you from investing in stocks or other assents because of the perceived risks (even if you know that it may bring you wealth in the long run). But your greed will drive you towards spending the money on a better lifestyle like buying a bigger house (which may also mean higher mortgage and utility bills).

Eventually, poor and middle-class people end up working for money, and the rich are looking for ways money can work for them.

This brings us to the next big idea.

It’s Not How Much Money You Make. It’s How Much Money You Keep.

“If you want to be rich, this is all you need to know. It is rule number one. It is the only rule. This may sound absurdly simple, but most people have no idea how profound this rule is. Most people struggle financially because they do not know the difference between an asset and a liability.”

Assets and liabilities. Do you know the difference? In simple words, an asset brings you money, and a liability takes money out of your pocket. And if you want to grow your wealth, you need to buy more assets and keep liabilities and expenses low.

Here is one of the key ideas of the book:

“Rich people acquire assets. The poor and middle class acquire liabilities that they think are assets.”

Guess what many people think is an asset, but it’s actually a liability? Their house! And it’s not only because of higher mortgage and utility bills:

“The greatest losses of all are those from missed opportunities. If all your money is tied up in your house, you may be forced to work harder because your money continues blowing out of the expense column, instead of adding to the asset column, the classic middle-class cash flow pattern.”

Question for you: is your house an asset or liability? ☺ Is it the right time to get a bigger house?

Start Acquiring Assets Early in Life.

“Keep expenses low, reduce liabilities, and diligently build a base of solid assets. For young people who have not yet left home, it is important for parents to teach them the difference between an asset and a liability. Get them to start building a solid asset column before they leave home, get married, buy a house, have kids, and get stuck in a risky financial position, clinging to a job, and buying everything on credit.”

That’s all about teaching your kids the “rich people mindset” and helping them develop financial IQ . That’s something I wish I had learned when I was much younger.

So here is what can go on the assets column:

- “Businesses that do not require my presence I own them, but they are managed or run by other people. If I have to work there, it’s not a business. It becomes my job.

- Stocks

- Bonds

- Income-generating real estate

- Notes (IOUs)

- Royalties from intellectual property such as music, scripts, and patents

- Anything else that has value, produces income or appreciates, and has a ready market.”

And nowadays, it’s so much easier to invest in all of those things than it was ten years ago. So no excuses. Encourage your kids to create assets (blogs, music, art, code, app – whatever) and teach them to be smart about the money they earn.

How to teach kids this concept? Well, in The Secrets of Happy Families, Bruce Feiler shares excellent ideas on this:

- Show them the money – talk to your kids about your finances, about your investments and debts (assets and liabilities).

- Give your kids allowances, provide them with the framework on what they can do with the money (e.g. spend, save, give away, share) and let them practice.

- Encourage kids to work, so they can learn different skills very early and have some money to practice.

If they make a mistake and lose the money – discuss the lessons learnt.

And, of course, never stop learning and educating yourself about money.

P.S.: Imagine if you would invest the money you spent on booze (that “one more drink”) when you were a student in S&P100…the average annual return for the S&P 500 in the 50-year period from 1970 to 2020 has been 10.83%…

Financial IQ is Crucial For Financial Independence.

“Without this financial knowledge, which I call financial intelligence or financial IQ, my road to financial independence would have been much more difficult.”

The right mindset is always a good starting point. But if you want to grow your wealth, you need to work your financial IQ first. Before investing any money, it is wise to educate yourself in four areas of expertise:

1. Accounting – “Accounting is financial literacy or the ability to read numbers. This is a vital skill if you want to build an empire…Financial literacy is the ability to read and understand financial statements which allows you to identify the strengths and weaknesses of any business.”

2. Investing – “Investing is the science of “money making money.” This involves strategies and formulas which use the creative right-brain side.”

3. Understanding markets– “Understanding markets is the science of supply and demand. You need to know the technical aspects of the market, which are emotion-driven, in addition to the fundamental or economic aspects of an investment. Does an investment make sense or does it not make sense based on current market conditions?”

4. The law – “A corporation wrapped around the technical skills of accounting, investing, and markets can contribute to explosive growth. A person who understands the tax advantages and protections provided by a corporation can get rich so much faster than someone who is an employee or a small-business sole proprietor.”

That’s the foundation, and if you get it right, the wealth-growing thing becomes easier and doesn’t look like rocket science. The key point is never to stop learning and put your knowledge into practice to grow your wealth. And it’s ok to make mistakes as long as you learn from them.

Also, in the book, Kiyosaki shares a great lesson about the power of corporation: rich people hold their assets in corporations to optimise taxes and grow their wealth. In summary, here is the difference:

| Business Owners with Corporations | Employees Who Work for Corporations |

| 1. Earn

2. Spend 3. Pay Taxes |

1. Earn

2. Pay taxes 3. Spend |

That’s why many wealthy people don’t show off their big fat personal bank statements – they have all of their money in corporations.

Fear of Losing The Money

“We all have tremendous potential, and we all are blessed with gifts. Yet the one thing that holds all of us back is some degree of self-doubt. It is not so much the lack of technical information that holds us back, but more the lack of self-confidence. Some are more affected than others.”

Lack of self-confidence = fear.

So question for you – What would you do if you weren’t afraid?

Have a think.

Kiyosaki says:

“The fear of losing money is real. Everyone has it. Even the rich. But it’s not fear that is the problem. It’s how you handle the fear. It’s how you handle losing. It’s how you handle failure that makes the difference in one’s life. That goes for anything in life, not just money. The primary difference between a rich person and a poor person is how they handle that fear.”

How are you handling your fear of failure? Are you approaching it like a winner with a growth mindset?

Focus

“If you have little money and you want to be rich, you must first be ‘focused,’ not ‘balanced.’ If you look at anyone successful, at the start they were not balanced. Balanced people go nowhere. They stay in one spot. To make progress, you must first go unbalanced. Just look at how you make progress walking.”

FOCUS: Follow One Couse Until Successful. Love it.

“The sun’s rays do not burn until brought to a focus.”

So instead of putting a few eggs in different baskets, put a lot of your eggs in a few baskets and FOCUS.

Learners Are Earners (In The Long Run)

“I recommend to young people to seek work for what they will learn, more than what they will earn. Look down the road at what skills they want to acquire before choosing a specific profession and before getting trapped in the Rat Race.”

It’s cool to be great at one thing, but when it comes down to making money – it’s important to learn other skills as well. And the best time to learn all of those skills is while you are still young. So think strategically – which skills do you need to earn more money in the future? Go and learn them! One by one. For some job experience, you’ll not get much money, but you’ll gain invaluable experience and develop the skills that will help you grow your wealth over time. That’s all about delayed gratification.

In pretty much every chapter, Kiyosaki highlights that we should always invest in our education:

“In reality, the only real asset you have is your mind, the most powerful tool we have dominion over.”

Your mind is your ASSET. And you always have a choice what to put in your brain – invest in learning a new skill or just sit on a couch and scroll through the social media feed. As Darren Hardy says in The Compound Effect:

“In essence, you make your choices, and then your choices make you.”

So make your choices wisely.

“I Can’t Afford It” vs “How Can I Afford It?”

“Rich dad believed that the words “I can’t afford it” shut down your brain. “How can I afford it?” opens up possibilities, excitement, and dreams.”

Mindset shift ☺ A little bit of greed changes the perspective. Brilliant.

And there is no progress without this little greed – we need the desire for something better to move forward.

So question for you – what do you want that you can’t afford (yet)? Have a think HOW can you afford it? Maybe use the WOOP technique for this:

W (wish)_____________________

O (outcome)__________________

O (obstacles)__________________

P (plan)___if_______then________

Give What You Want To Get!

“Whenever you feel ‘short’ or in ‘need’ of something, give what you want first and it will come back in buckets. That is true for money, a smile, love, friendship. I know it is often the last thing a person may want to do, but it has always worked for me. I just trust that the principle of reciprocity is true, and I give what I want.”

That is brilliant. Good stuff always comes back. Want more respect from your kids? Give them this respect first. Want more attention from your partner? Give them some attention first. Want to succeed in your career? Help others to succeed. Works pretty much all the time.

Action Steps For You

- Create an excel sheet (or use an app) and track your monthly expenses and income, as well as your assets and liabilities. Assess what is working and what is not working;

- Develop a plan on how you can grow your assets and take action (e.g. learn about popular investment strategies and start investing – property, stocks, crypto, etc.);

- Teach financial literacy to your kids and help them grow their assets early in life.

Quotes from the book: